We discuss below key FSIE and BEPS 2.0 developments, including the potential considerations for Labuan entities.

1. Changes to FSIE regime in Hong Kong and Malaysia

The European Code of Code Group (Business Taxation) (EUCOCG) is mandated by the European Council to promote and strengthen good tax governance both within the European Union (EU) and at the international level. Amongst its many functions, the EUCOCG maintains the EU list of non-cooperative jurisdictions for tax purposes (EU List), with blacklisted jurisdictions potentially being subject to both tax and non-tax defensive measures by EU Member States, such as withholding tax measures, non-deductibility of payments to a blacklisted jurisdiction and denial of EU funding.

In 2021, the EUCOCG had highlighted concerns in the FSIE regime of several countries, including Hong Kong and Malaysia. As a result, these countries made changes to their FSIE regimes, as discussed briefly below:

Hong Kong

Hong Kong has implemented sweeping changes to its tax treatment of foreign-sourced income, effective from 1 January 2023. Previously, Hong Kong generally did not tax foreign income. Under the refined regime, foreign-sourced passive income received by a Hong Kong company in Hong Kong will be subject to tax. This includes interest, dividends, disposal gains in relation to shares or equity interests and income from intellectual property.

However, foreign-sourced dividend or interest income may continue to be exempted from tax in Hong Kong subject to various conditions, such as the fulfilment of economic substance, nexus or participation requirements.

Hong Kong, like Malaysia, does not tax capital gains1. Hence, it is interesting to note that foreign disposal gains from the sale of equity interests will now be subject to Hong Kong tax if remitted into Hong Kong, unless the relevant FSIE conditions are met. In fact, Hong Kong has received feedback from the EU that the scope of its foreign sourced income taxation should be expanded to cover a wider range of foreign disposal gains, and Hong Kong is now revisiting its position based on this feedback.

1Malaysia does however impose Real Property Gains Tax (“RPGT”) on the disposal of real property in Malaysia or real property company (“RPC”) shares

Malaysia

Prior to 1 January 2022, foreign sourced income received in Malaysia by any person, other than a Malaysian resident company conducting banking business, insurance or sea or air transport, was exempt from tax. From 1 January 2022, this blanket exemption was removed for Malaysian residents. Conditional exemptions have since been introduced. For Malaysian resident companies, the exemption only applies to foreign-sourced dividend income, where various conditions are met.

Initially, the Malaysian company only needed to demonstrate that its foreign dividend income had been received from a jurisdiction with a headline tax rate of at least 15% and that foreign tax had been suffered on the dividend income or the profits from which the dividend income was paid, for the exemption to apply. However, in December 2022, an additional condition was introduced, such that the recipient of the dividend income must also comply with economic substance requirements in Malaysia for the exemption to be available.

In the Council of the European Union “Outcome of proceedings” memorandum dated 14 February 2023, it was stated that Hong Kong and Malaysia have been given until 30 April 2023 to adapt their legislations in relation to FSIE. Hence, it is possible that further refinements will be forthcoming.

2. Labuan IBFC’s unique value proposition in global investment holding structures

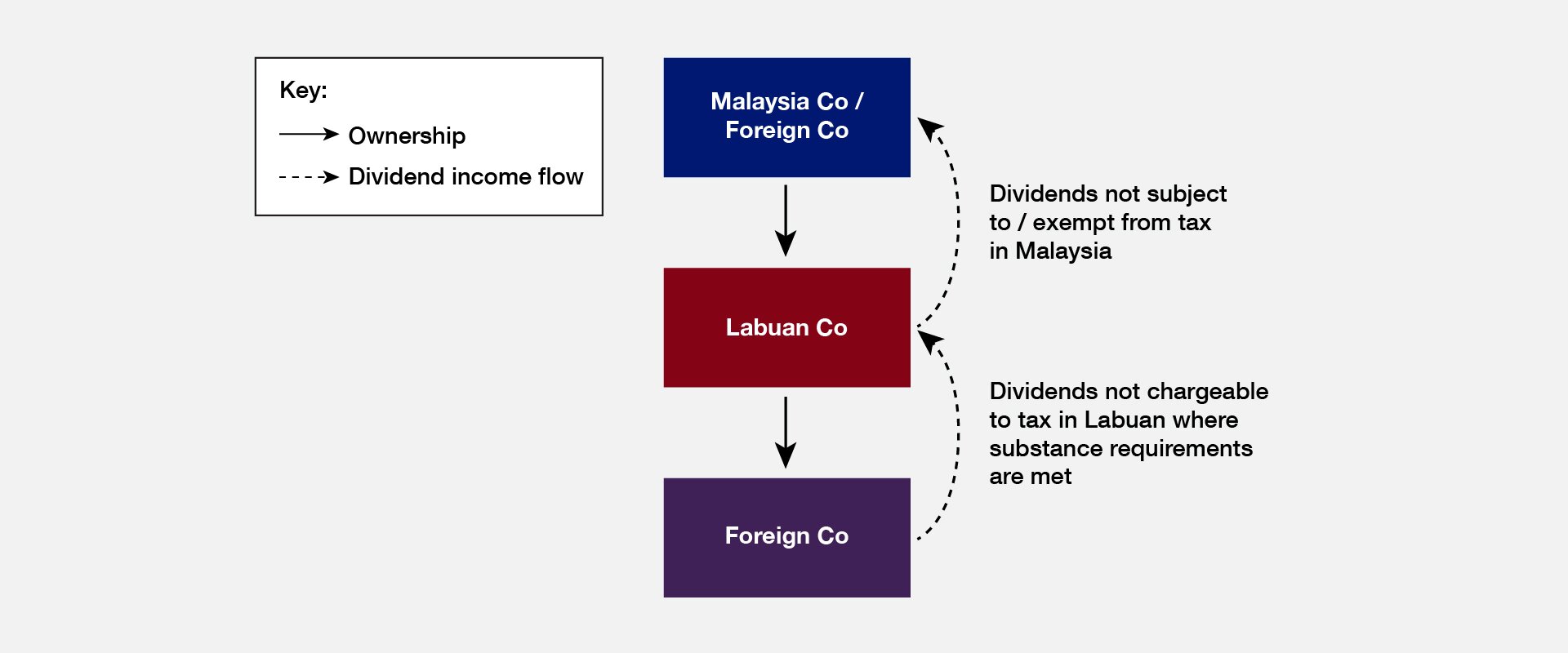

Labuan IBFC offers an enticing value proposition for global investment holding structures through its unique taxation regime and wide range of entity-types. It is worth noting that at this time, the EUCOCG deems Labuan IBFC as a compliant jurisdiction with no pending commitments – which further amplifies the jurisdiction’s value proposition.

A Labuan investment holding company only holding shares in other companies and earning only dividends and/or capital gains, i.e. a “pure equity holding company”, is not chargeable to tax in Labuan (including on its dividend income received from outside Malaysia), provided that the following conditions are met:

- The Labuan company incurs at least MYR20,000 (approximately USD4,600) of annual operating expenditure in Labuan; and

- The Labuan company exercises its control and management in Labuan. This would include holding a directors’ meeting in Labuan at least once a year.

Further, dividends declared by such Labuan company to its immediate holding company should be exempt from tax in Malaysia. A simple illustration of the above holding structure is depicted below:

It would be remiss to discuss international tax developments without also discussing BEPS 2.0 implementation.

Briefly, there have been significant developments on the implementation of BEPS 2.0 globally, which include:

- On 15 December 2022, the Council of the European Union unanimously adopted a Directive ensuring a global minimum tax for multinational enterprise groups and large-scale domestic groups in the EU. EU Member States have until 31 December 2023 to transpose this EU Directive into relevant domestic legislation. The rules will start to become effective for fiscal years starting on or after 31 December 2023.

- On 16 December 2022, the Swiss parliament passed the constitutional amendment which details the inclusion of Pillar Two into Swiss domestic law. Consequently, the proposed constitutional amendments will be subject to a mandatory public vote on 18 June 2023, before Pillar Two can be fully implemented in Switzerland.

- On 16 December 2022, Japan released the 2023 tax reform proposal indicating its commitment to the implementation of Pillar Two. These changes are likely to take effect from 1 April 2024 onwards. Other aspects of Pillar Two are being considered for legislation in the 2024 tax reform. Japan is also closely monitoring international tax developments, in shaping its tax policy.

- On 20 December 2022, Indonesia issued Government Regulation No. 55 (GR-55) detailing several tax provisions, including the intention to implement BEPS 2.0 in its tax system. Further details are expected to be released later in the year of 2023.

- On 23 December 2022, the Korean legislature passed Pillar Two legislation, which is to come into force effective 1 January 2024. With this, Korea becomes the first country to implement Pillar Two rules into its domestic legislation.

- On 14 February 2023, in its 2023 national budget Singapore announced that a 15% minimum tax in accordance with Pillar Two would be introduced for large multinational enterprises, for financial years starting on or after 1 January 2025. Singapore will continue to monitor international developments and will adjust the implementation timeline as needed if there are delays internationally.

- On 22 February 2023, Hong Kong announced during its 2023/2024 budget that Pillar Two would be implemented in Hong Kong starting from 2025 onwards. In various seminars held following the re-tabling of Malaysia’s Budget 2023 on 24 February 2023, it was stated that Malaysia will seek to introduce Pillar Two starting from the year 2024.

Large multinational groups should assess whether they will suffer top-up taxes under Pillar Two rules and must be prepared to comply with filing and administrative requirements. An immediate starting point would be to undertake an ETR impact assessment exercise, to identify jurisdictions in which the ETR is below 15% as well as information and data gaps.

As governments around the globe work to implement Pillar Two, it is useful to consider how this will impact Labuan. We set out some points below in this regard.

- Pillar Two will generally only impact multinational groups with a group turnover of EUR750 million or more (“in-scope MNE Groups”). As such, Labuan entities which are parts of smaller groups would not be impacted.

- “Excluded” dividend income and “excluded” equity gains or losses, as defined, would be excluded from the Pillar Two income used to calculate the ETR. As such, pure equity holding companies holding shares in subsidiaries may not be impacted, even if they are part of in-scope MNE Groups.

- Labuan will be included as part of Malaysia when calculating the jurisdictional ETR for a multinational group. As such, a Labuan entity which is part of an in-scope MNE group would consolidate its results with all other group entities in Malaysia when calculating its jurisdictional ETR for Malaysia. Hence, where the group also has Malaysian companies which are subject to tax at the usual Malaysian corporate tax rate at 24% and/or which have significant substance in Malaysia which qualify for the substance-based income exclusion, there may be little or no top-up tax. This is subject of course to a detailed analysis of the group’s specific facts and circumstances.

This article contains information in summary form and is therefore intended for general informational purposes only. It is not intended to be a substitute for detailed research or the exercise of professional judgment.